A typical downpayment on a house would be about 15% of its price. It may vary depending upon the type of loan, lender, and mortgage. Getting a loan with a lower down payment can help you get to your goal of homeownership more quickly, but you'll also pay more in interest over time.

Because of student debt and credit card debt, first-time buyers are often challenged with saving for a downpayment. There are many government-backed programs available that will help you save for a down payment. These include VA and USDA loans.

Your mortgage payment will generally be lower if you have a higher down payment. If you can afford 20% down, private mortgage insurance will cost you about 1% per year.

Before you begin looking for a house, it is a good idea to start saving for the down payment. You can use a savings account, a high-interest online bank account or even a second mortgage to put money aside for the down payment.

The average down payment on a house has risen over the past decade, according to real estate firm Redfin. During the pandemic sell-off, it went up from 10% and 15%.

The rise in home prices has made it more difficult for many homebuyers to afford a house. This led to many bidding wars, and buyers paying more for homes than the list price.

A large downpayment is a sign that your seriousness about purchasing a home. This could increase your chances to get the home you want, and it may also reduce the number or competing offers.

A high down payment also shows that you're financially responsible, so it's a good sign for sellers. This is especially true when you live in large cities. A larger down payment can indicate that your ability to maintain and take care of the property.

Although the down payment for a house has been high in recent years it is expected to drop soon. Some metros, like San Francisco, Seattle and Denver, have seen downpayments drop or stay the same compared to a year ago. However, other cities, like Riverside, Calif. and Denver have seen their downpayments increase.

What is the average down payment for a house in 2019

The typical down payment on a house in July was $62,500, up 13.6% from a year earlier. This is nearly twice the amount of the median downpayment of $32,917, which was a year before. It's also the highest it's been in five decades.

When the housing market is hot it's common to see downpayments go up and down. However, when the market slows down it is important to understand what's going on at the local level.

Redfin examined 40 metros and found that seven saw a decline. Riverside was the most affected, with a down payment of $55,000. This is 15.4% less than a year ago. San Francisco followed closely with $364,000 as the average down payment. This was 7.8% less than one year earlier.

FAQ

How much will it cost to replace windows

Window replacement costs range from $1,500 to $3,000 per window. The total cost of replacing all of your windows will depend on the exact size, style, and brand of windows you choose.

What are the top three factors in buying a home?

The three most important things when buying any kind of home are size, price, or location. It refers specifically to where you wish to live. The price refers to the amount you are willing to pay for the property. Size refers how much space you require.

What flood insurance do I need?

Flood Insurance protects from flood-related damage. Flood insurance can protect your belongings as well as your mortgage payments. Find out more about flood insurance.

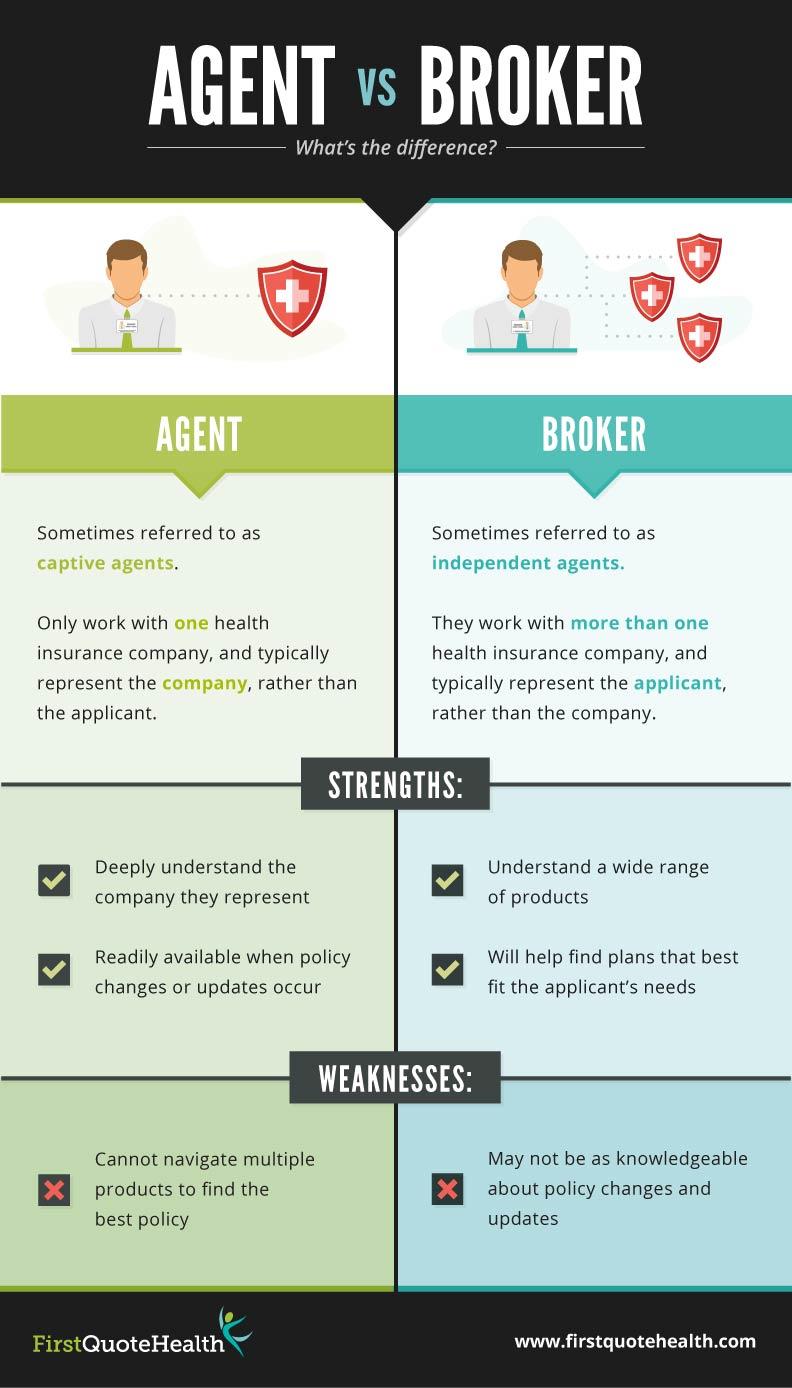

Should I use an mortgage broker?

If you are looking for a competitive rate, consider using a mortgage broker. Brokers are able to work with multiple lenders and help you negotiate the best rate. Brokers may receive commissions from lenders. Before signing up for any broker, it is important to verify the fees.

How long does it take for my house to be sold?

It depends on many factors, such as the state of your home, how many similar homes are being sold, how much demand there is for your particular area, local housing market conditions and more. It may take 7 days to 90 or more depending on these factors.

What are the benefits of a fixed-rate mortgage?

With a fixed-rate mortgage, you lock in the interest rate for the life of the loan. You won't need to worry about rising interest rates. Fixed-rate loans offer lower payments due to the fact that they're locked for a fixed term.

Statistics

- Over the past year, mortgage rates have hovered between 3.9 and 4.5 percent—a less significant increase. (fortunebuilders.com)

- Based on your credit scores and other financial details, your lender offers you a 3.5% interest rate on loan. (investopedia.com)

- When it came to buying a home in 2015, experts predicted that mortgage rates would surpass five percent, yet interest rates remained below four percent. (fortunebuilders.com)

- This seems to be a more popular trend as the U.S. Census Bureau reports the homeownership rate was around 65% last year. (fortunebuilders.com)

- Private mortgage insurance may be required for conventional loans when the borrower puts less than 20% down.4 FHA loans are mortgage loans issued by private lenders and backed by the federal government. (investopedia.com)

External Links

How To

How to find real estate agents

Real estate agents play a vital role in the real estate market. They help people find homes, manage their properties and provide legal advice. The best real estate agent will have experience in the field, knowledge of your area, and good communication skills. To find a qualified professional, you should look at online reviews and ask friends and family for recommendations. It may also make sense to hire a local realtor that specializes in your particular needs.

Realtors work with sellers and buyers of residential property. A realtor's job is to help clients buy or sell their homes. Apart from helping clients find the perfect house to call their own, realtors help manage inspections, negotiate contracts and coordinate closing costs. A commission fee is usually charged by realtors based on the selling price of the property. Some realtors do not charge fees if the transaction is closed.

There are many types of realtors offered by the National Association of REALTORS (r) (NAR). To become a member of NAR, licensed realtors must pass a test. A course must be completed and a test taken to become certified realtors. NAR designates accredited realtors as professionals who meet specific standards.